Table of contents

What Is the 50/30/20 Rule on a Budget Template? (Explained for Nonprofits)

Meta Title: What Is the 50/30/20 Rule on a Budget Template? (Explained for Nonprofits)

Meta Description: Learn how the 50/30/20 budgeting rule works, why it matters for nonprofit budgets, and how to apply it using Actually Finance.

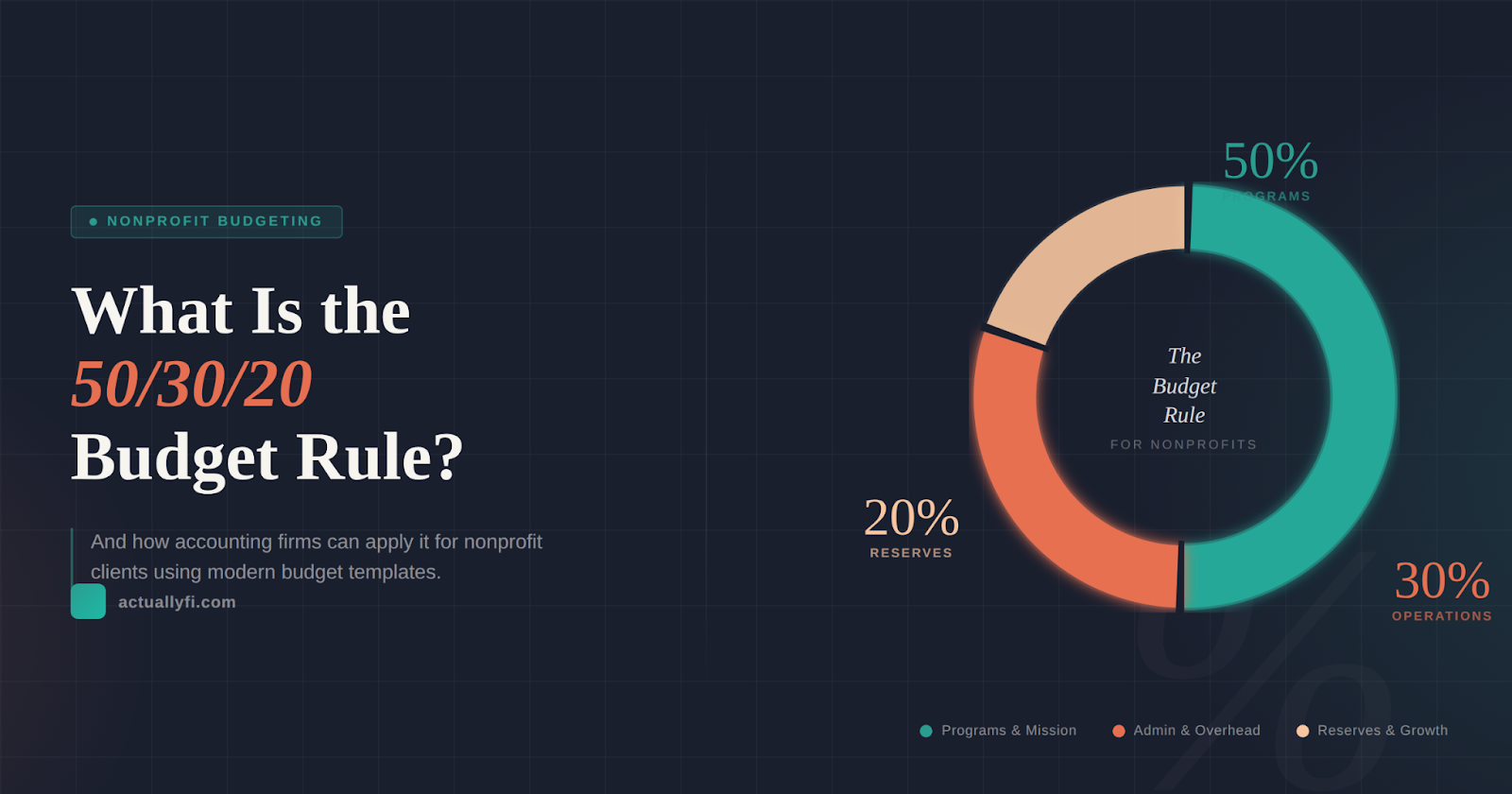

What Is the 50/30/20 Rule?

The 50/30/20 rule is a simple budgeting framework that divides total income into three key spending categories: - 50% Needs: Essential operating costs (e.g., rent, salaries, utilities) - 30% Wants: Strategic or discretionary spending (e.g., marketing, staff development) - 20% Savings or Goals: Long-term reserves, investments, or debt reduction. This model was popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan and is widely used in personal finance to maintain balance and sustainability. While it was designed for individuals, the 50/30/20 framework can also help nonprofits structure their budgets around core priorities and financial health.

How the 50/30/20 Rule Translates to Nonprofits

Nonprofits operate differently than households, but the logic behind the rule still applies — it encourages balanced allocation across essential operations, growth initiatives, and long-term stability.

Instead of “wants,” think of this as mission expansion. Nonprofits that dedicate a consistent percentage to reserves and growth are more resilient to funding fluctuations

Benefits of Using the 50/30/20 Framework in Nonprofit Budgeting

• Encourages balance: Prevents overspending on admin or underfunding programs.

• Simplifies decision-making: Helps boards and leadership prioritize spending.

• Promotes sustainability: Builds reserves to weather grant delays or emergencies.

• Improves transparency: Donors see a clear and rational allocation of funds.

It's not a one-size-fits-all model, but it provides a strong baseline for discussions around program funding, operational efficiency, and financial planning.

How to Use the Rule in Google Sheets or Templates

If you're building your budget manually, you can apply the 50/30/20 rule using a simple formula:

=Total Revenue * 50%

=Total Revenue * 30%

=Total Revenue * 20%

Then assign your expense categories accordingly.

You can start with these free templates: - Google Sheets Budget Template Gallery - Smartsheet Nonprofit Budget Template - Vertex42 Budget Worksheet

However, spreadsheets can quickly become messy when multiple team members edit them or when you need to track restricted vs. unrestricted funds.

If you use QuickBooks for your accounting, see our complete guide to budgeting for nonprofits in QuickBooks for step-by-step budget setup.

Applying the 50/30/20 Rule with Actually Finance

Actually Finance takes the simplicity of frameworks like 50/30/20 and makes them actionable at the program and grant level.

With Actually Finance, nonprofits can:

- Build and adjust program-level budgets following 50/30/20 principles.

- Track actual vs. budget automatically by grant, fund, or department.

- Visualize spending breakdowns to ensure balance between operations, mission, and reserves.

- Collaborate with finance teams and accountants using real-time dashboards.

This turns the 50/30/20 concept from a theoretical guide into a living financial model your whole team can understand.

When to Adjust the Rule

Not every nonprofit should follow the 50/30/20 split exactly. Adjust the percentages based on your stage and funding mix:

- Early-stage nonprofits: May spend 60–70% on program development and outreach.

- Established organizations: Can reserve closer to 20–25% for long-term sustainability.

- Grant-heavy nonprofits: Should align reserves with grant cycles and reporting requirements.

The key is consistency and intentionality — not rigid adherence.

The Bottom Line

The 50/30/20 rule provides an easy starting point for nonprofit budgeting: fund your mission first, invest in growth second, and build financial stability third.

By blending this timeless budgeting concept with modern tools like Actually Finance, your organization can bring clarity, collaboration, and confidence to every financial decision.

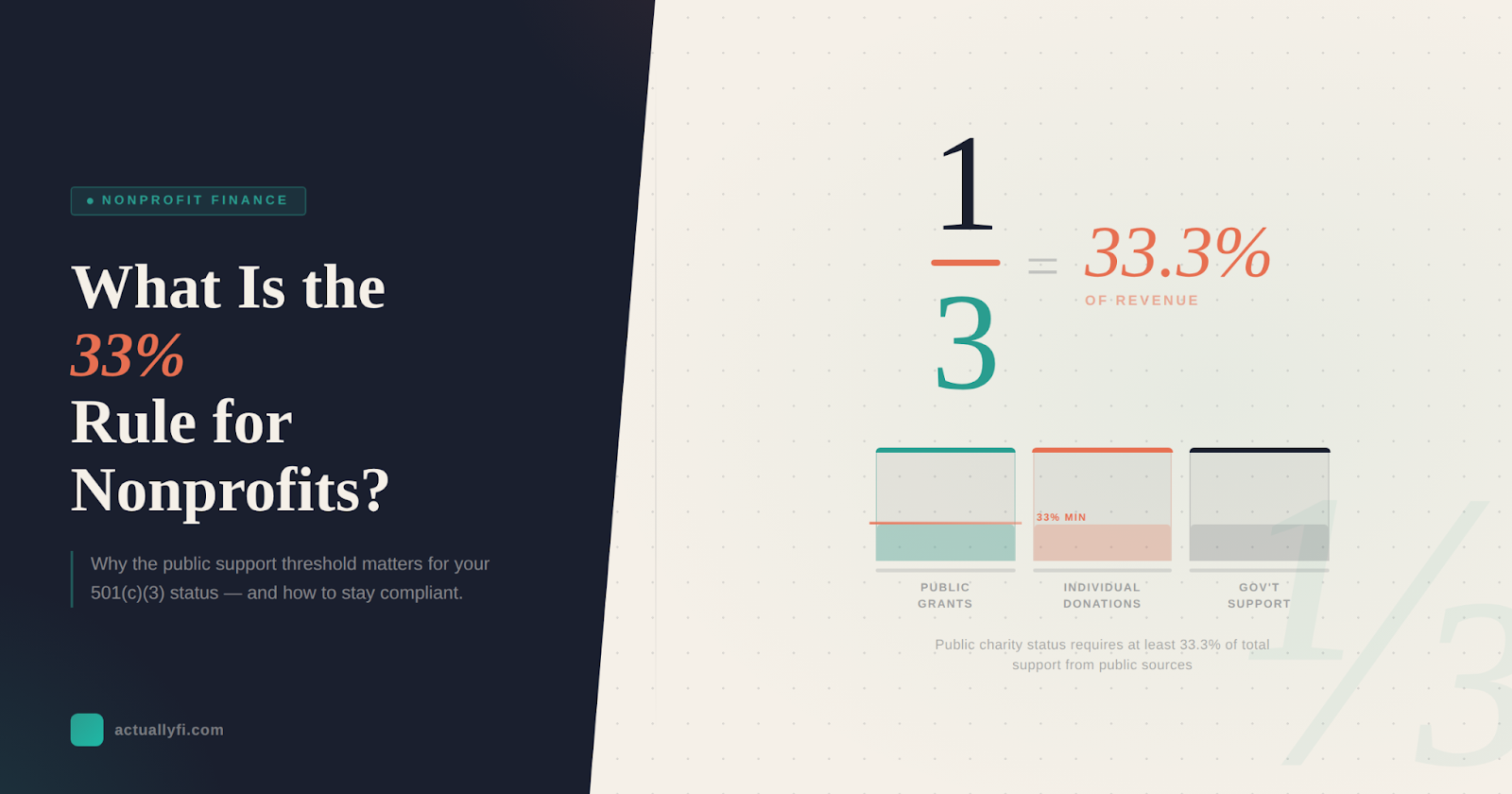

Make sure your funding sources meet compliance requirements too — read about the 33% public support test for nonprofits.

Want a deeper dive into nonprofit budgeting? Check out our article here Nonprofit Budgeting Template.

Frequently Asked Questions About the 50/30/20 Rule for Nonprofits

Can nonprofits use the 50/30/20 rule for grant budgeting?

Yes, the 50/30/20 framework can be adapted for grant budgets by allocating 50% to direct program costs, 30% to program expansion or indirect costs, and 20% to administrative reserves. However, always follow the specific requirements outlined in your grant agreement, as funders may have their own allocation guidelines.

What is the difference between the 50/30/20 rule and program budgeting?

The 50/30/20 rule is a high-level allocation framework that divides total revenue into three broad categories. Program budgeting goes deeper by assigning specific dollar amounts to individual programs, grants, or initiatives. Many nonprofits use both approaches together — the 50/30/20 split as a strategic guideline and program budgets for detailed planning.

Is the 50/30/20 rule required for nonprofits?

No, the 50/30/20 rule is a guideline, not a legal requirement. There is no IRS mandate to follow this specific split. Nonprofits should adapt the percentages based on their stage, mission, funding mix, and donor expectations.

How do I adjust the 50/30/20 split for a startup nonprofit?

Early-stage nonprofits often need to invest more heavily in program development and outreach. A common adjustment is 60–70% on programs, 20% on growth and capacity building, and 10–20% on reserves. As the organization matures and stabilizes, you can gradually shift toward the standard 50/30/20 split.

David Cristello

.svg)

About the Author

David Cristello is the Co-Founder of Actually Finance. He's been an entrepreneur in the accounting and nonprofit space for over 10 years, previously building a company that made the Inc5000 list

.png)

.png)

.png)