1. What Is Program Budgeting? (In Plain English)

2. Why Move to Program Budgeting?

3. Essential Components of Program Budgets

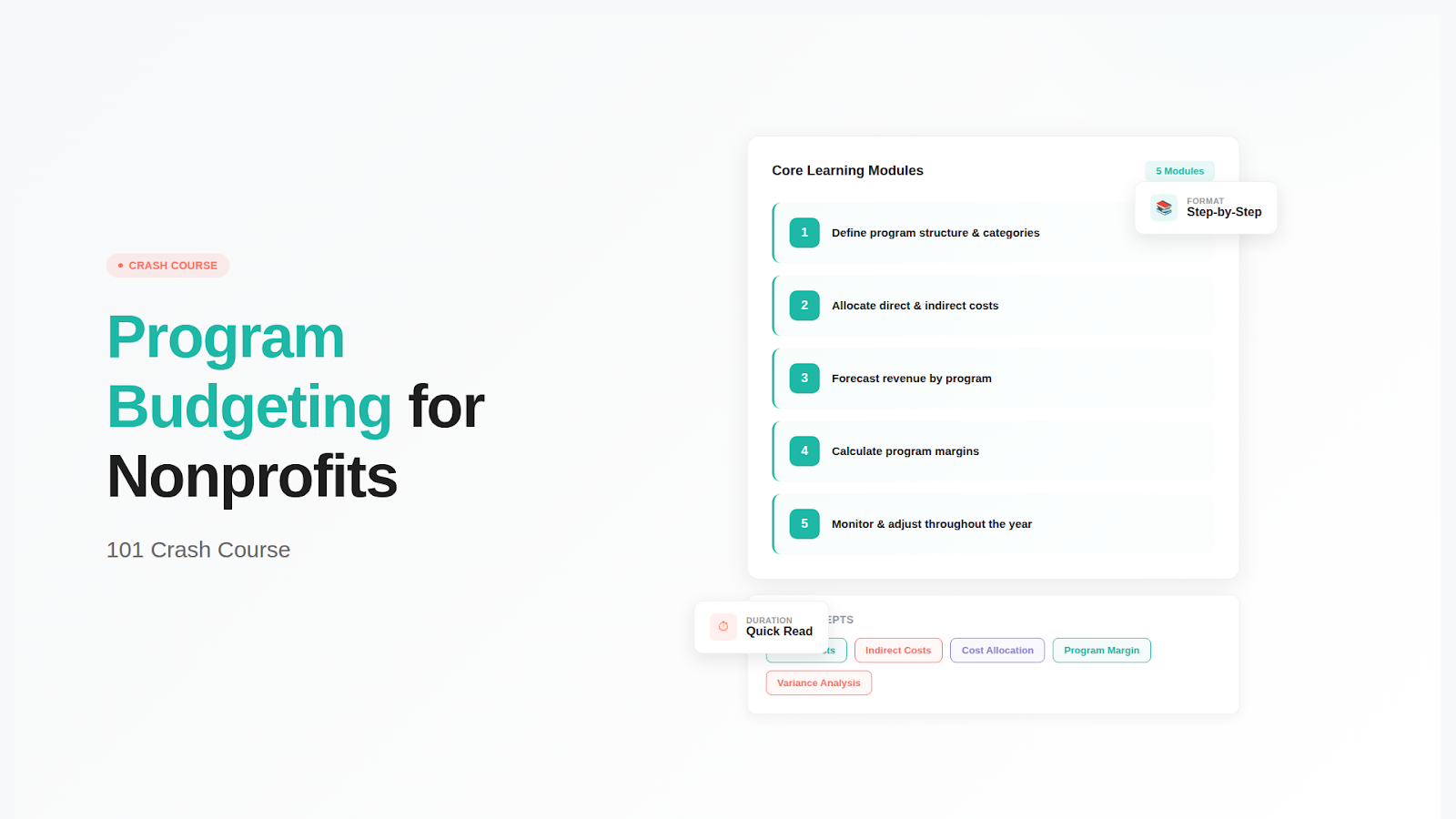

4. Step-by-Step: Creating Your Program Budget

5. Managing Cash Flow in Program Budgets

6. Conclusion and Next Steps

Table of contents

Last updated: March 17, 2026

Program budgeting for nonprofits is critical, albeit not very glamorous. Nonprofits start to serve a mission and track things like meals served, youth trained, families housed, and animals rescued.

And yet, behind every successful program is a clear, intentional budget… one that connects dollars to mission outcomes. Many nonprofits operate with stretched resources, making effective budgeting critical for achieving their missions.

Program budgeting for nonprofits is the method that makes this link visible.

Budgets should be treated as living documents and integrated into the nonprofit's financial activities throughout the year.

Unlike a general nonprofit's budget, which covers all organizational activities, program budgets break down how restricted and unrestricted funds will support specific programmatic goals and deliverables. As part of nonprofit budgeting, this approach also helps manage financial uncertainties by preparing for unexpected challenges. Documenting and sharing the finalized budget with your team fosters transparency and trust among stakeholders. Monitoring revenue and expenses should be part of the nonprofit's culture, involving everyone in the budgeting process (a practice essential to all types of nonprofit organizations). Involve key stakeholders (such as program managers, executive leadership, and board members) in the budgeting process to ensure comprehensive input and alignment.

What You'll Learn:

- Create accurate program budgets that satisfy funder requirements

- Allocate indirect costs properly using federally approved methods

- Ensure grant compliance through proper cost categorization

- Track program financial performance against budgeted projections

- Understand the key components of a nonprofit budget

What Is Program Budgeting? (In Plain English)

Program budgeting is simply building your budget around the core programs or services your nonprofit delivers. Instead of one total expense line for salaries or supplies, program budgeting asks:

- How much does each program cost?

- What revenue supports each one?

- Can we continue delivering this program sustainably?

For example, a youth services nonprofit might build separate budgets for:

- After school tutoring

- Summer leadership camp

- College access program

Each has its own revenue streams and its own cost structure. That level of clarity gives leaders a deeper view of what's driving impact alongside what needs attention.

It is essential to identify and diversify income sources, including contributed income, and assess their reliability for both restricted and unrestricted funding. These budgets also enable nonprofit organizations to calculate actual program costs, measure program-specific return on investment, and allocate resources strategically across multiple initiatives.

Why Should Nonprofits Use Program Budgeting?

Oftentimes, moving to a program budget isn't a choice ... it's a requirement by funders. Even if it's not a strict requirement, the board should be pushing for this clarity. In other words, program budgeting for your nonprofit will surface eventually, and it's much better to get a head start (both for governance and for better strategic fundraising and decision-making). The National Council of Nonprofits recommends program budgeting as a best practice for financial management and funder accountability.

Related: Within your budget, you'll want to assign a contingency fund of 5-10% of your annual budget to cover unexpected expenses.

If you've always budgeted at the organization level, you may wonder why you'd bother to slice the work into separate programs. The answer usually shows up the moment your board, a donor, or a grantor asks:

"How much does it cost to run this specific program?"

Or:

"Are we losing money on that service?"

Without program budgets, the best you can do is estimate. Program budgeting eliminates the guessing.

A few key benefits:

✅ True cost visibility

Some programs attract revenue but quietly drain resources. Others lose money but are vital to the mission. Program budgets reveal both.

✅ Better grant storytelling

Funders love details so they know where their money is going. There's a big difference between:

"This program costs $215 per student per month," is much more compelling than "Support our youth program."

✅ Stronger strategy

Program budgeting makes tough decisions informed, not emotional. It gives leaders the data to grow the right initiatives and sunset those no longer generating impact. By supporting forecasting and scenario modeling as part of broader organization plans, program budgeting enhances financial stability and enables more strategic decision-making.

✅ Improved staff engagement

Program managers can take ownership when they see budgets tied to their decisions and outcomes.

What Is the Difference Between a Program Budget and an Operating Budget?

A program budget details the financial requirements for a specific initiative or project, while a nonprofit operating budget encompasses all organizational revenue and expenses across programs, administration, and fundraising. Program budgets typically span shorter timeframes (one to three years) and focus on restricted funds designated for particular purposes. In contrast, operating budgets cover the full fiscal year and include both restricted and unrestricted funds.

The budget planning process for a nonprofit is closely tied to its broader plans and strategic objectives. You cannot function effectively without understanding program budgets.

Program budgets connect to operating budgets because they represent detailed components of the larger organizational financial plan, showing how resources support specific programmatic goals within the nonprofit's strategic plan.

What Are the Essential Components of a Program Budget?

At its core, you'll want to manage direct costs and indirect costs. For your program manager, they'll care about direct costs since they can control those (indirect costs are often things like rent, etc).

In addition to core program costs, program budgets should also account for fundraising and marketing expenses, and, when applicable, potential revenue from ticket sales.

Direct Costs

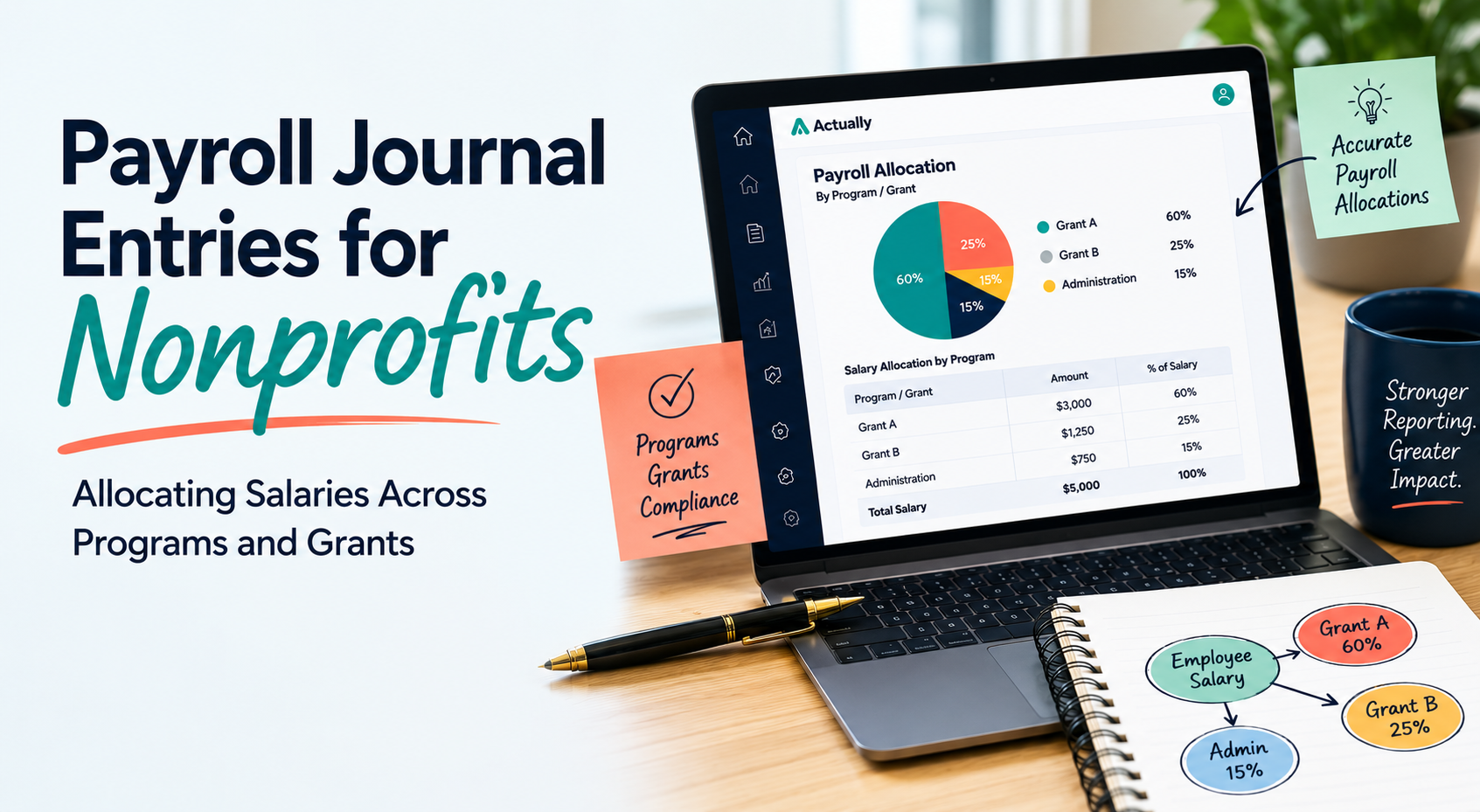

Personnel Costs

Staff salaries represent the largest expense category in most nonprofit program budgets, calculated by multiplying each employee's annual salary by the percentage of time they dedicate to the specific program. Benefits typically add 25-35% to salary costs (which includes things like health insurance, retirement, payroll taxes, etc).

Program Operations

Direct expenses are what is required to fulfill the services. These are things like staff salaries, supplies, and anything else that goes into the delivery of the program.

Equipment purchases or rentals specific to the program must be justified by program needs and align with funder guidelines on allowable capital expenses versus operating costs.

In sum, these are common direct costs:

- Program-specific staff and contractors

- Supplies and materials

- Event or activity costs

- Travel directly supports program services

If the expense disappears when a program stops, it's a direct cost.

How Does Indirect Cost Allocation Work for Nonprofits?

Administrative costs are allocated to programs using either the organization's federally negotiated indirect cost rate or the 10% de minimis rate under 2 CFR 200.414 (typically 10% of modified total direct costs). This allocation covers facility costs, administrative staff time, financial management systems, and other overhead expenses that support program operations.

Unlike direct costs, which are easily attributable to specific programs, indirect costs are allocated using standardized methodologies approved by funders to ensure a consistent and fair distribution of shared organizational expenses across all programs. The Uniform Guidance (2 CFR Part 200) provides the federal framework for how nonprofits must handle cost allocation for grants.

A fair allocation method may be based on:

- Staff time percentage

- Square footage used

- Enrollment headcount

Key Points:

- Personnel costs typically represent 60-80% of total program expenses

- Operating expenses can be estimated using a roll-forward budgeting process as a starting point (and then adjusting as necessary)

- Indirect cost rates must follow federal guidelines and funder requirements

Step-by-Step: How to Create Your Nonprofit Program Budget

When to use this: For new grant applications, program expansions, or annual program planning cycles.

- Define Program Scope: Document specific activities, deliverables, target populations, and timelines to establish the foundation for all budget calculations.

- Calculate Personnel Costs: Multiply actual employee salaries by the program's full-time equivalent (FTE) percentage, then add benefits at your organization's standard rate.

- Estimate Operations: Base program expenses on historical financial data for similar activities or obtain current vendor quotes for materials, supplies, and services.

- Apply Indirect Rate: Multiply total direct costs by your organization's federally negotiated indirect cost rate or use the 10% de minimis rate if no negotiated rate exists.

- Create Budget Narrative: Develop written justifications for each major cost category that explain how expenses directly support program goals and comply with funder guidelines.

- Final Review: With your final budget nearly ready to go, sanity check the numbers against the funder requirements and organizational capacity.

Comparison: Federal Grant vs. Foundation Grant Budgets

How Do Nonprofits Manage Cash Flow in Program Budgets?

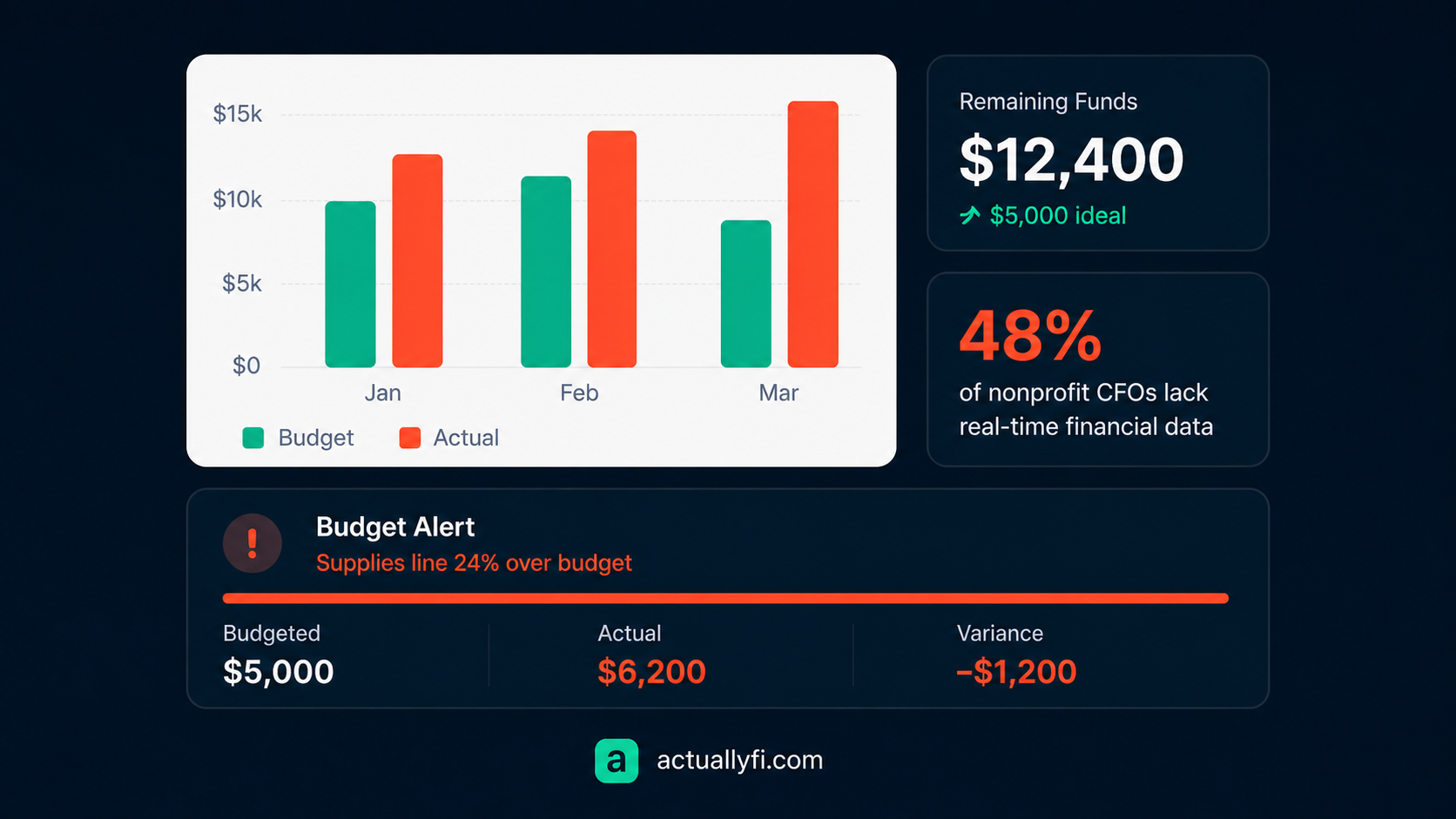

Nonprofit organizations should review and adjust on a recurring basis (depending on the frequency of change, this can be monthly or quarterly).

While it can be a pain to review budgets this frequently, the pain of missing your numbers is a lot worse. Plus, you'll start to gain superpowers by seeing in advance challenges in support and program delivery.

Cash flow management is especially critical for grant-funded programs because many grants operate on a reimbursement basis. This means your organization must spend money upfront and then submit expense reports to get reimbursed, which can take 30 to 90 days. Without a cash reserve or line of credit, this timing gap can leave programs unable to cover payroll or vendor invoices even when the grant funds are fully approved.

Protip: Create a cash reserve to protect from changes in your income (funding). Map out each grant's payment schedule alongside your monthly expenses so you can anticipate and plan for any gaps.

Setting Financial Goals for Programs

When setting financial goals for programs, nonprofit organizations should ensure alignment with their overall strategic plan and the specific objectives of each initiative.

By defining and tracking these financial goals, nonprofits can make data-driven decisions about resource allocation, prioritize funding for high-impact activities, and demonstrate financial success to stakeholders and funders. Clear financial goals also support long-term planning and help ensure that each program contributes to the organization's mission and economic sustainability.

Incorporating Capital Budgets for Special Initiatives

Capital budgets are an important component of the budgeting process as it allows for more long term, strategic investments that go beyond the daily operating expenses in a typical program budget.

When incorporating capital budgets into the overall budgeting process, nonprofits should carefully assess the long-term impact and sustainability of each investment. This includes evaluating potential risks, estimating future maintenance or replacement costs, and considering how the investment aligns with the organization's strategic plan. For example, a nonprofit may develop a capital budget to fund the construction of a new community center or to purchase cloud-based accounting software that enhances financial management capabilities.

By integrating capital budgets into their financial planning, nonprofit organizations can make informed decisions about major expenditures, ensure proper allocation of resources, and support the successful execution of special initiatives that drive organizational impact.

Leveraging Budgeting Software for Program Management

Of course you'll use Excel. We love Excel (sort of) and I'm sure you do too.

That said, Excel breaks down quickly by not having great version control, feeding actuals into the budget, or generating reporting out of the box. Once you've established the time and priority to make an effective budget, we strongly suggest budgeting tools (of course, we have our own but you can also compare against other ones).

Addressing Fundraising Costs in Program Budgets

Fundraising costs are an important part of any nonprofit program budget. These expenses may include staff salaries, marketing and communications, event costs, and donor management systems. Much like admin costs, you'll want to allocate fundraising expenses across programs using a consistent methodology, such as percentage of revenue generated or direct solicitation hours.

Most funders expect fundraising overhead to stay within 15-25% of total expenses. Tracking your cost-to-raise-a-dollar ratio by program helps you demonstrate efficiency and identify where your fundraising efforts are most effective. If a specific program's fundraising costs exceed what's reasonable, that's a signal to evaluate the strategy or diversify funding sources for that initiative.

A Simple Example: Animal Rescue Program Budget

Let's say your animal rescue runs two primary programs:

- Shelter Operations

- Community Pet Support Workshops

You might discover:

- Shelter operations cost more than donations cover but they fulfill your core mission.

- Workshops nearly break even and help attract new supporters.

With that insight, you could:

- Seek more restricted grants for shelter care

- Invest in expanding the workshop model

- Communicate your actual cost of rescue more confidently

Program budgeting turns gut feelings into informed strategy.

Challenge 1: Accurate Cost Allocation Across Multiple Programs

Solution: Implement time tracking systems for all staff and develop documented allocation methodologies that clearly specify how shared costs are distributed among programs.

Use project codes in your accounting software to automatically track direct expenses by program, and conduct quarterly allocation reviews to ensure accuracy and adjust for changes in program activities or staffing.

Challenge 2: Compliance with Varying Funder Requirements

Solution: Make sure you have a simple, easily referenceable "Funder Requirement" overview. This should include allowable costs (and other things, like indirect rate limits, matching fund requirements, and even reporting due dates).

Maintain separate budget versions tailored to different funder guidelines while ensuring all versions roll up to your master program budget for internal tracking and organizational financial planning.

Challenge 3: Managing Budget Changes During Program Implementation

Solution: Build 5-10% contingency funds into initial program budgets where funder guidelines permit, and establish formal change management procedures that specify when budget modifications require funder approval.

Document variance thresholds (typically 10% between budget categories) and maintain regular communication with funders about program changes that may affect budget allocations or timelines.

Frequently Asked Questions About Nonprofit Program Budgeting

What is the difference between a program budget and a line-item budget?

A program budget organizes expenses by the specific programs or services your nonprofit delivers, showing the true cost of each initiative. A line-item budget groups expenses by category (salaries, rent, supplies) across the entire organization without tying them to specific programs. Program budgets give you deeper insight into which programs are sustainable and help satisfy funder reporting requirements.

How often should nonprofits review their program budgets?

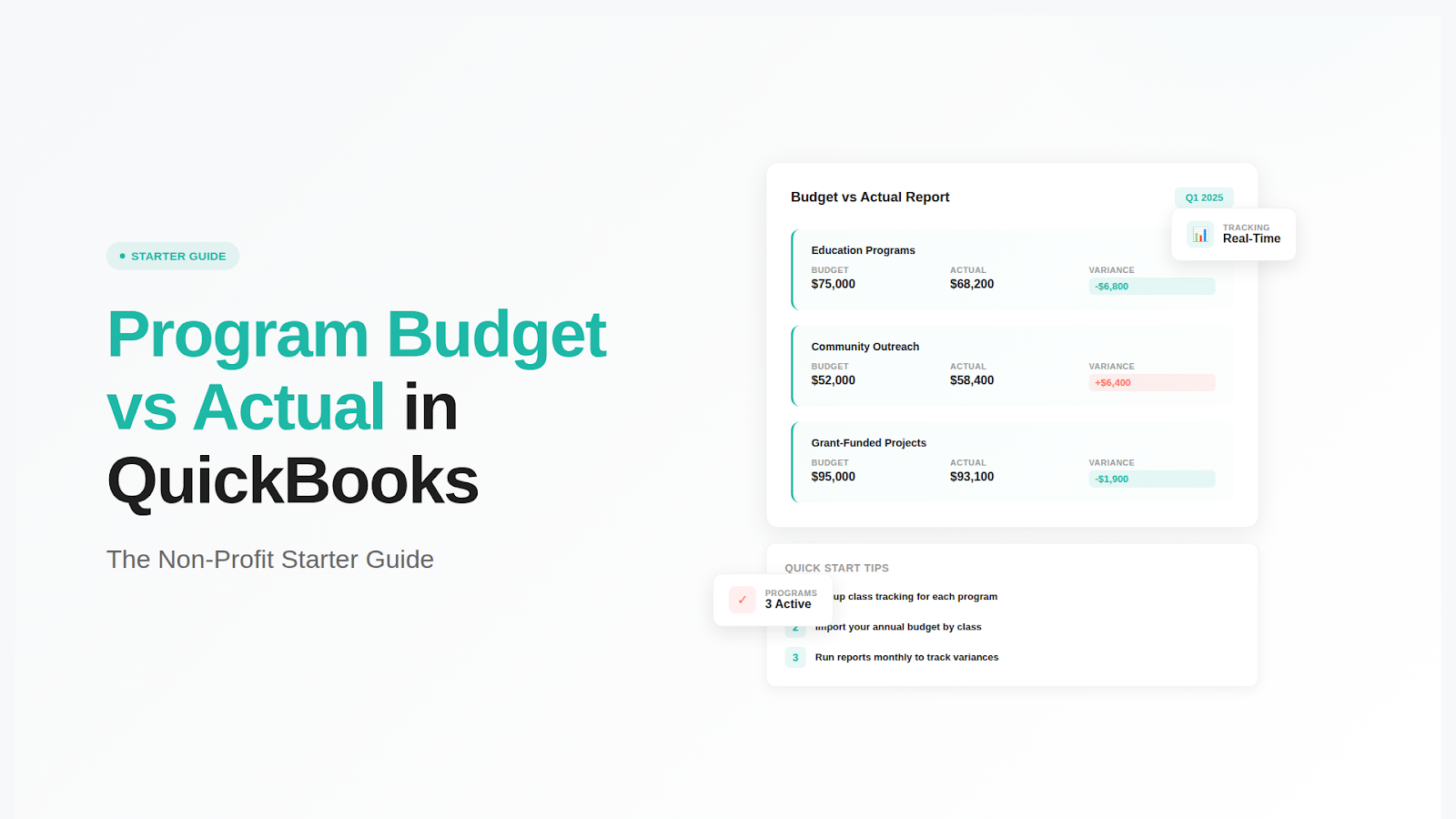

Nonprofits should review program budgets at least quarterly, though monthly reviews are ideal for programs with high spending velocity or multiple funding sources. Regular reviews help catch variances early, ensure grant compliance, and allow for timely budget modifications before small issues become major problems.

What is a de minimis indirect cost rate?

The de minimis indirect cost rate is a federally approved 10% rate that nonprofits can use if they have never had a federally negotiated indirect cost rate. It is applied to modified total direct costs and covers overhead expenses like rent, utilities, and administrative support. This rate is available to all nonprofits receiving federal funding under the Uniform Guidance (2 CFR 200).

How do you allocate shared staff costs across multiple programs?

Shared staff costs are allocated based on the percentage of time each employee dedicates to each program. This requires a time-tracking system where staff log hours by program. The percentage is applied to total compensation (salary plus benefits) to determine the amount charged to each program budget. Many funders require documented timesheets or effort certifications to support these allocations.

What should be included in a budget narrative for a grant application?

A budget narrative should explain and justify each major cost category in your program budget. It should describe why each expense is necessary, how it was calculated, and how it directly supports program goals. Include details like staff roles and FTE percentages, the basis for cost estimates, how indirect costs are calculated, and any in-kind contributions or matching funds.

Can program budgets help with fundraising?

Yes. Program budgets are powerful fundraising tools because they demonstrate exactly how donor dollars will be used. They allow you to tell compelling cost-per-outcome stories (e.g., "$215 per student per month") rather than making vague appeals. Program budgets also help identify funding gaps for specific initiatives, making grant applications and donor pitches more targeted and credible.

Why does program budgeting fail in most nonprofits?

Program budgeting fails when organizations treat it as a one-time exercise instead of a living process. The most common breakdown happens when budgets are built during grant season and never revisited. Without ongoing tracking, real-time data, and regular variance reviews, budgets quickly become outdated and get ignored. Success requires integrating program budgets into monthly financial routines and giving program managers ownership of their numbers.

Is program budgeting enough without funding visibility?

No. A program budget without real-time funding visibility is guesswork. Teams need to see what's been committed, what's been spent, and what's remaining across every grant and revenue source at any given moment. Without that clarity, even a well-built budget can't prevent overspending, missed deadlines, or misallocated funds. Pairing program budgets with tools that provide live funding data is what turns a static plan into an actionable financial strategy.

What are the biggest mistakes nonprofits make when budgeting?

The most common mistakes include underestimating indirect costs, budgeting in silos without cross-departmental input, skipping cash flow planning, and failing to update budgets as conditions change. Many nonprofits also neglect to build contingency funds, rely too heavily on a single revenue source, or treat budgets as a compliance exercise rather than a strategic tool. Avoiding these pitfalls starts with making budgeting a collaborative, ongoing process rather than an annual checkbox.

Conclusion and Next Steps

Effective program budgeting enables nonprofit organizations to create accurate grant applications, maintain proper financial stewardship of restricted funds, and demonstrate measurable program impact to current and prospective funders.

To get started:

- Review your current program budgets for accuracy and compliance with funder requirements, identifying any gaps in cost allocation or documentation.

- Implement time-tracking systems to improve direct cost attribution and develop written procedures for indirect cost allocation.

- Create standardized budget templates for different funder types to streamline future grant applications and ensure consistent financial reporting.

Additional Resources

- National Council of Nonprofits - Budgeting for Nonprofits: Best practices and guidance on nonprofit financial management, budgeting processes, and board financial oversight.

- 2 CFR Part 200 - Uniform Administrative Requirements (Uniform Guidance): The federal framework governing cost principles, audit requirements, and administrative standards for grants and agreements.

- Propel Nonprofits - Nonprofit Budget Template: A downloadable budget template with built-in formulas for revenue, expenses, and program-level tracking.

- Grants.gov - OMB Uniform Guidance for Grants: Official federal resource for understanding grant policies, compliance requirements, and application procedures.

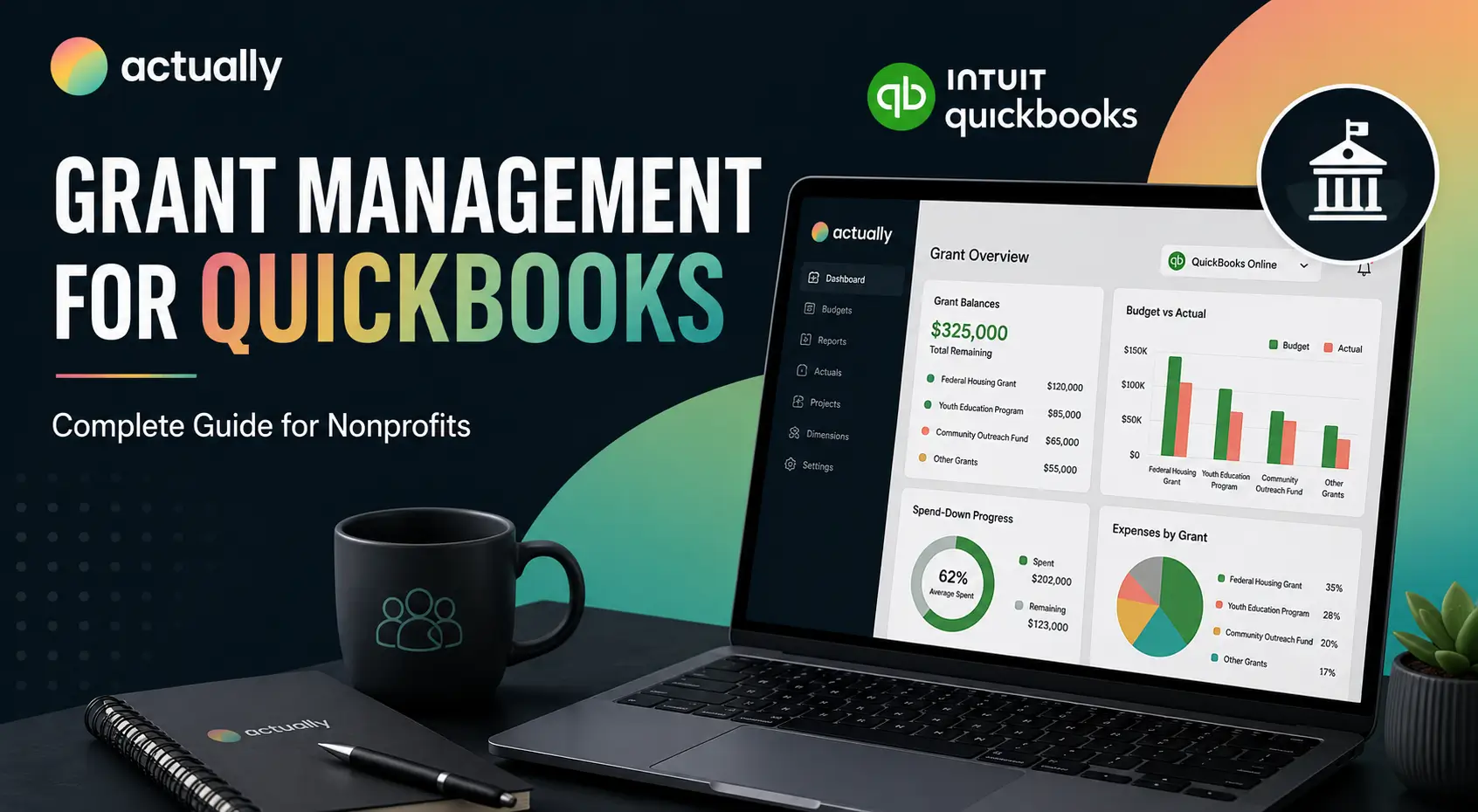

- Look at budgeting tools like Actually - software that gives nonprofits real-time budget visibility, grant spend tracking, and funding clarity integrated with QuickBooks Online.

David Cristello

.svg)

About the Author

David Cristello is the Co-Founder of Actually Finance. He's been an entrepreneur in the accounting and nonprofit space for over 10 years, previously building a company that made the Inc5000 list

.png)

.webp)