Table of contents

If you run a nonprofit, there's a number the IRS cares about more than almost anything else on your Form 990: 33⅓%. That's the threshold for the public support test, and falling below it can change your organization's legal classification overnight.

We've talked to nonprofit finance directors who didn't know this test existed until their accountant flagged it during tax prep. By then, they'd already spent two years leaning too heavily on a single foundation grant. The fix wasn't hard, but the stress was avoidable.

This guide breaks down what the 33% rule actually means, how the IRS calculates it, common traps that catch nonprofits off guard, and what to do if you're close to the line.

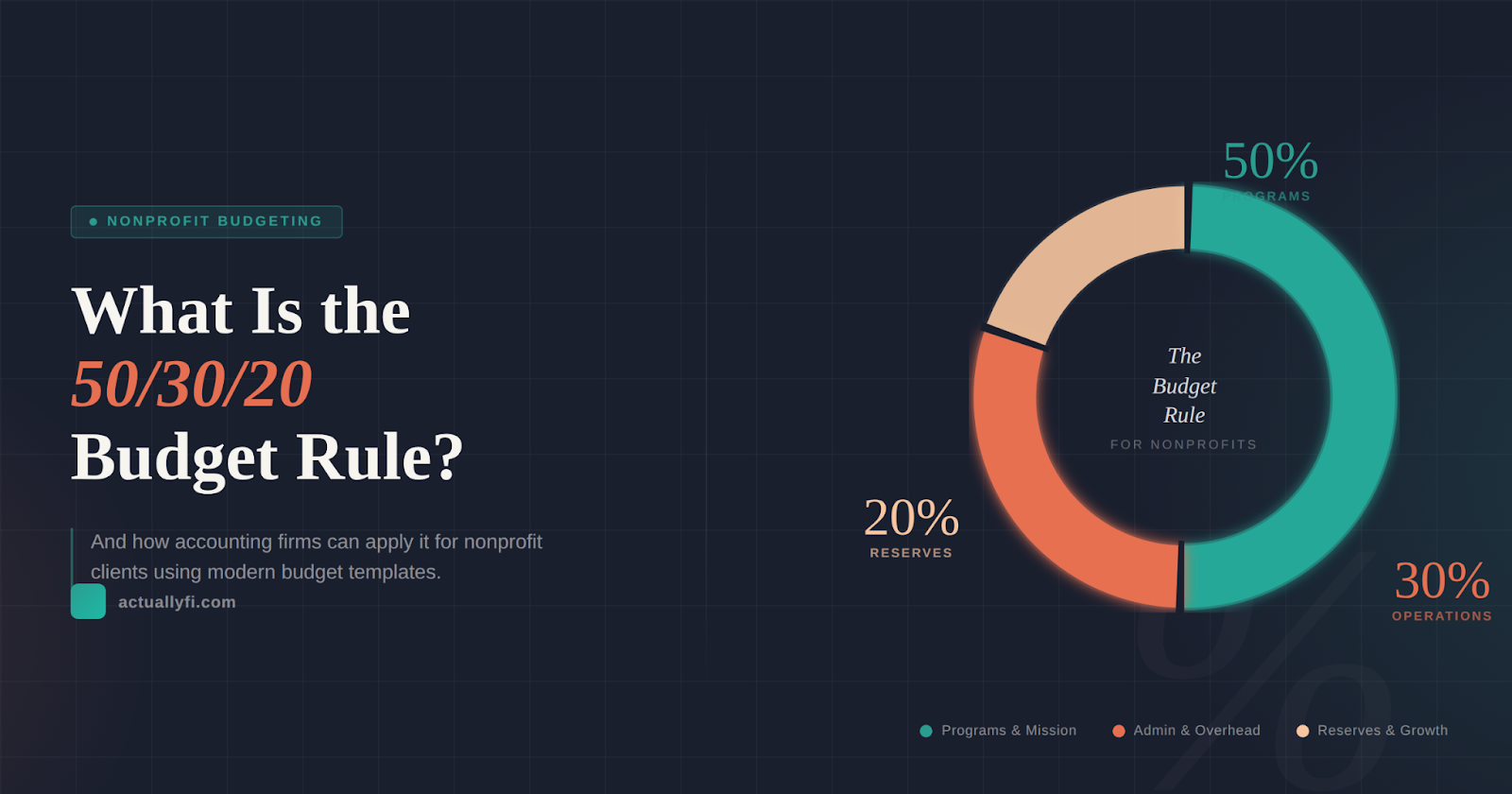

What Is the 33% Rule for Nonprofits?

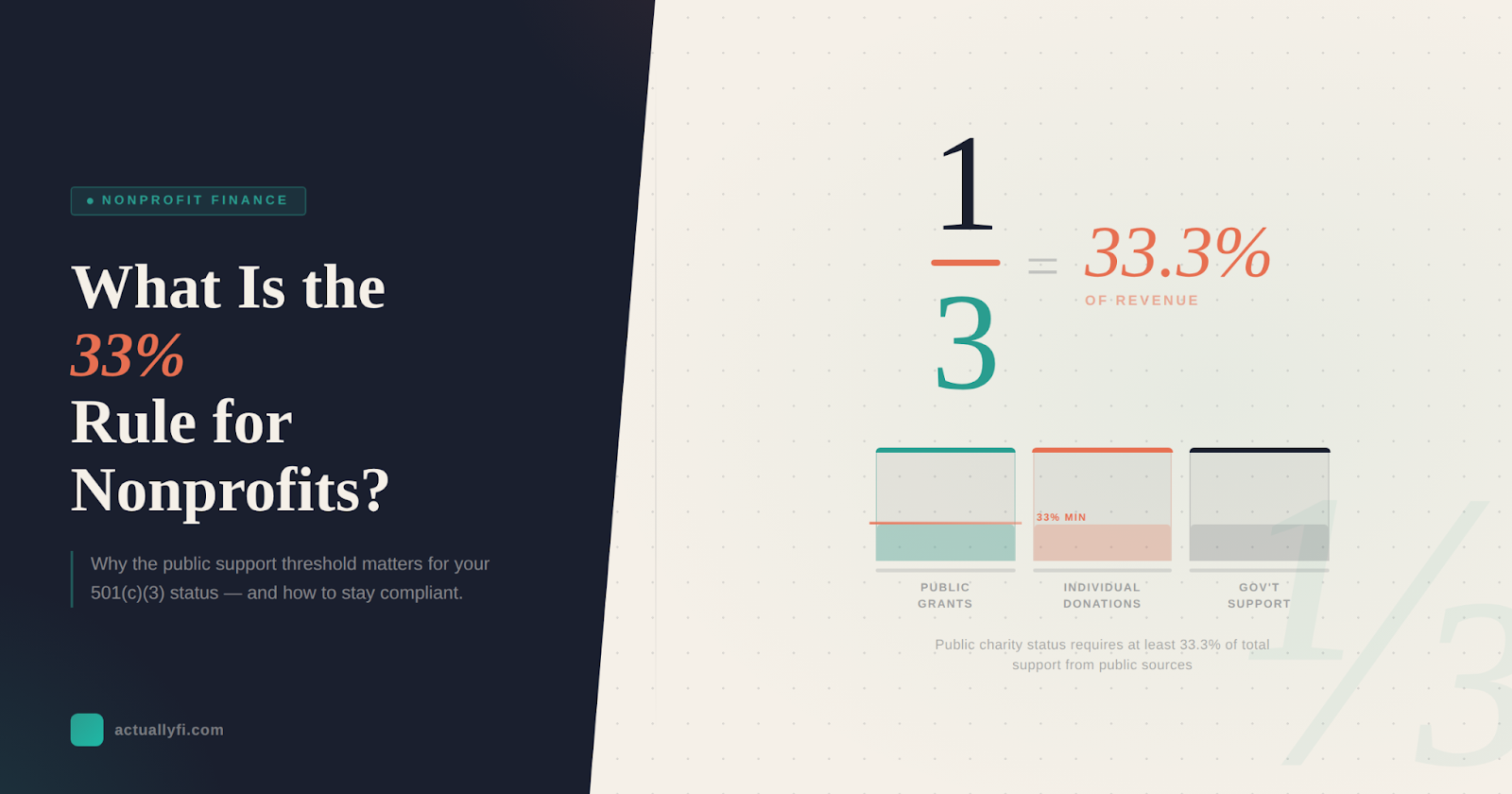

The 33% rule — formally called the public support test — determines whether your nonprofit qualifies as a public charity or gets reclassified as a private foundation.

According to the IRS Public Support Test Guide, a 501(c)(3) organization must receive at least one-third (33⅓%) of its total financial support from public sources to maintain public charity status.

"Public sources" includes individual donors, other public charities, government grants and contracts, corporations, and community foundations. The key word is broad — the IRS wants to see that your funding comes from a wide base of supporters, not a handful of large checks.

If more than two-thirds of your funding comes from a small number of private donors or a single foundation, the IRS may reclassify you as a private foundation. That's not just a label change — it comes with excise taxes, stricter self-dealing rules, and mandatory payout requirements that fundamentally change how you operate.

Here's a quick way to think about it: if one donor disappeared tomorrow and it would crater your public support ratio, you have a concentration risk the IRS is specifically watching for.

Why the Public Support Test Exists

The distinction between public charities and private foundations goes back to the Tax Reform Act of 1969. Congress wanted to ensure that organizations benefiting from tax-exempt status were genuinely serving the public — not just operating as a tax-advantaged vehicle for a wealthy family or a single corporate donor.

The logic is straightforward: if a nonprofit draws support from hundreds or thousands of people, it's more likely accountable to the community. If it depends on one or two major funders, the power dynamic shifts, and the organization starts looking more like a private foundation regardless of its stated mission.

Failing the test doesn't mean the IRS shuts you down. But the consequences are real. Private foundations face a 1.39% excise tax on net investment income, strict limits on transactions with "disqualified persons" (board members, major donors, their families), and mandatory annual distributions of at least 5% of assets. For a lean nonprofit, these requirements can be genuinely burdensome.

Beyond the legal implications, losing public charity status can erode donor confidence. Many individual donors and some foundations specifically target public charities because of the higher deduction limits available. Reclassification can quietly reduce your fundraising effectiveness even if your mission hasn't changed at all.

How to Calculate Your Public Support Percentage

The formula itself is simple. The judgment calls around what counts are where it gets tricky.

Public Support % = (Public Contributions ÷ Total Support) × 100

Public Contributions includes donations from individuals, government grants, contributions from other public charities, and corporate gifts. Total Support includes all of the above plus investment income, membership dues, unrelated business income, and any other revenue.

The IRS doesn't look at a single year. They average your numbers over a rolling five-year period (technically, the current year plus the four preceding years), which smooths out one-off spikes or dips.

A Real Example

Say your nonprofit received $2 million in total support over five years. Of that, $800,000 came from a single private foundation. The remaining $1.2 million came from individual donors, government grants, and a community foundation.

Your public support percentage: $1.2M ÷ $2M = 60%. You're well above the 33⅓% threshold.

But here's the catch: the IRS applies a 2% limit rule. Any single donor's contributions that exceed 2% of your total support only count up to that 2% cap for the public support calculation. So if one individual gave $300,000 of your $2M total, only $40,000 (2% of $2M) counts as "public support" from that donor. The rest still counts in your total support denominator, which can pull your ratio down faster than you'd expect.

This is the detail that trips up most nonprofits — particularly those with a few very generous major donors.

Common Mistakes That Put Nonprofits at Risk

Over-reliance on a single funder. This is the most common issue we see. A nonprofit lands a large multi-year grant, it becomes 40-50% of total revenue, and nobody thinks about the public support ratio until year three. Even if a donor gives multiple smaller gifts over several years, the IRS aggregates them. One relationship can quietly dominate your support profile.

Ignoring in-kind donations. Non-cash gifts — donated office space, pro bono legal services, contributed supplies — count as public support when properly documented at fair market value. Many nonprofits leave these out of their calculations entirely, which means they're underreporting their public support percentage. If you're close to the threshold, properly valuing in-kind contributions might be what keeps you above it.

Misclassifying restricted vs. unrestricted funds. A restricted grant from a private foundation is still a contribution from that foundation for public support purposes — it doesn't magically become "public" because it funds a public-facing program. The restriction affects how you spend it, not how the IRS classifies the source.

Not running the numbers until tax time. The public support test should be something your finance team monitors quarterly, not something your accountant calculates once a year in March. By the time you discover a problem on the Form 990, you've already lost a year of potential corrective action.

Counting earned revenue incorrectly. Program service revenue (fees for services, ticket sales, tuition) generally does NOT count as public support. Many nonprofits assume all revenue helps their ratio, but earned income goes into the Total Support denominator without boosting the numerator. Growing your earned revenue without growing donor support actually lowers your public support percentage.

How to Track the 33% Rule Proactively

Spreadsheet tracking is better than nothing, but it's fragile. Formulas break, someone forgets to update a tab, and suddenly you're making strategic decisions based on stale numbers.

The most effective approach we've seen nonprofits use involves three things working together:

1. Tag every income source at the point of entry. When a donation or grant hits your books, classify it immediately — individual donor, government grant, private foundation, corporate gift, earned revenue. If you wait and try to categorize retroactively at year-end, you'll miss things.

2. Run quarterly ratio checks. Pull your five-year rolling totals every quarter and calculate where you stand. If you're trending below 40%, that's your early warning signal to diversify fundraising before it becomes urgent.

3. Use software that automates the math. Actually Finance connects to your QuickBooks data and tracks funding sources automatically, so you can see your public support ratio in real time without building custom spreadsheets. It also helps segment restricted vs. unrestricted funds, which feeds directly into accurate ratio calculations.

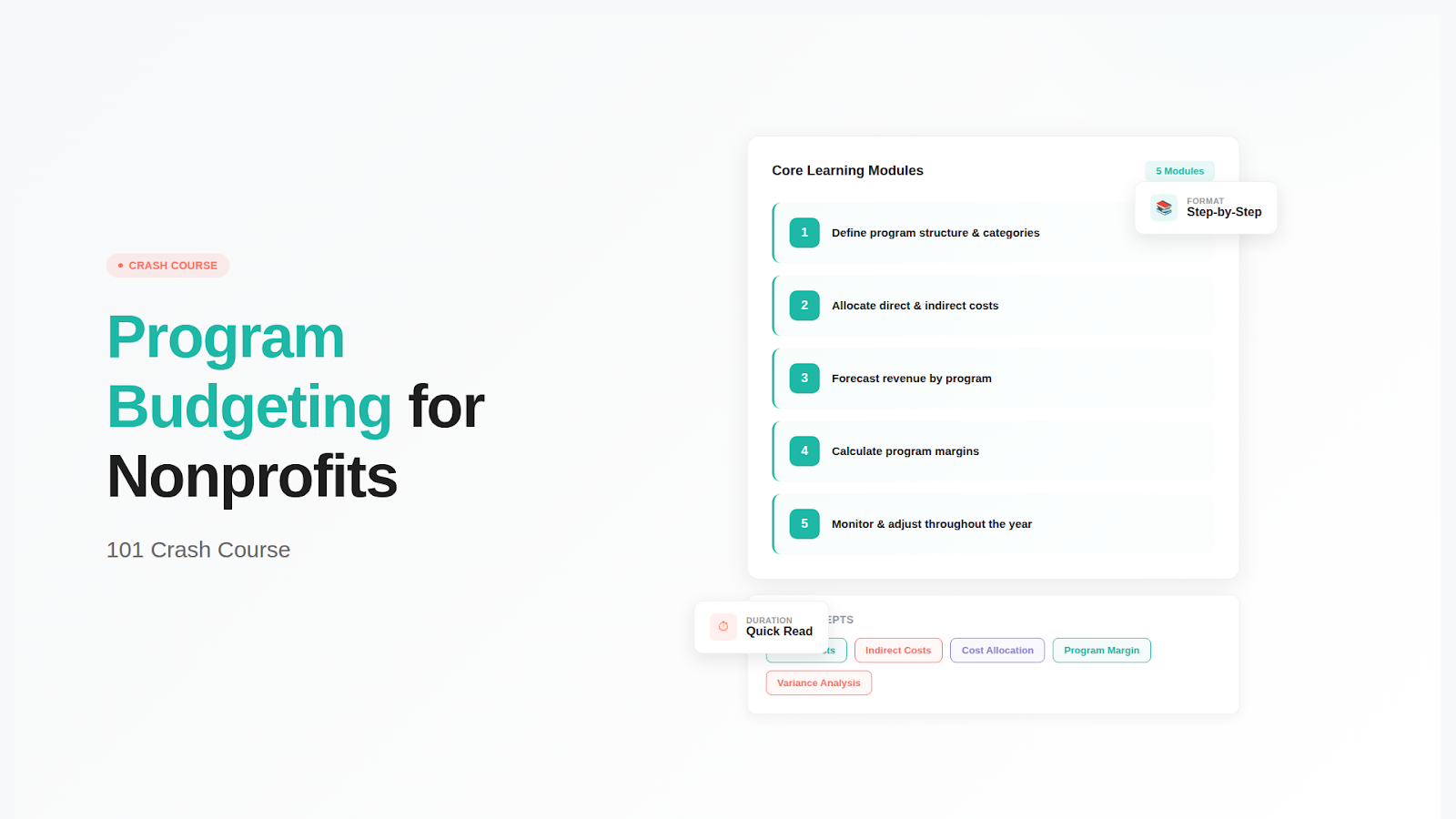

For a step-by-step guide to organizing your finances in QuickBooks to support this kind of tracking, see our complete guide to budgeting for nonprofits in QuickBooks.

What to Do If You're Below the 33% Threshold

First — don't panic. The IRS built flexibility into the system.

If your five-year average falls below 33⅓%, there's an alternative facts-and-circumstances test that can still qualify you as a public charity. Under this test, you need to meet a lower 10% threshold AND demonstrate factors like broad public engagement through volunteers, events, and community outreach, a consistent pattern of seeking diverse funding even if recent years dipped, alignment between your activities and genuine public benefit, and a governing body that represents broad community interests rather than a few donors.

This alternative test gives the IRS discretion, which means documentation matters enormously. If you're relying on it, keep detailed records of your fundraising efforts, volunteer programs, community events, and any media coverage or public engagement that demonstrates broad support.

The smarter long-term play is to diversify before you need to. If you see your ratio trending toward 35-38%, that's the time to invest in individual donor cultivation, apply for more government grants, or launch a small-dollar fundraising campaign. Waiting until you're at 30% means you're already in recovery mode.

Frequently Asked Questions About the 33% Rule

What happens if a nonprofit fails the 33% public support test?

The organization may be reclassified as a private foundation by the IRS. This triggers excise taxes on investment income, stricter rules on transactions with board members and major donors, and mandatory annual distributions. However, the IRS uses a five-year rolling average, so one bad year won't automatically disqualify you. There's also the alternative facts-and-circumstances test if you're between 10% and 33%.

How often does the IRS evaluate the public support test?

The IRS reviews it when your organization files its annual Form 990. They look at a rolling five-year window, which means the calculation shifts each year as the oldest year drops off and the current year is added. This rolling average protects organizations from being penalized for a single unusual year — like receiving an unexpectedly large bequest.

Do government grants count as public support?

Yes — federal, state, and local government grants generally count as public support. However, unusually large government grants may be subject to special rules. Specifically, any single grant that exceeds the greater of $5,000 or 1% of your total support may only partially count toward public support. The portion exceeding that threshold is excluded from the numerator but still counts in the denominator.

Can in-kind donations help meet the 33% threshold?

Absolutely. Donated goods, pro bono services, contributed use of facilities, and other non-cash gifts count as public support when documented at fair market value. For organizations that receive significant volunteer support or donated resources, proper documentation of in-kind contributions can meaningfully improve the public support ratio. Keep detailed records including donor acknowledgment letters, independent valuations for large gifts, and descriptions of services received.

David Cristello

.svg)

About the Author

David Cristello is the Co-Founder of Actually Finance. He's been an entrepreneur in the accounting and nonprofit space for over 10 years, previously building a company that made the Inc5000 list

.png)

.webp)