Table of contents

Most nonprofit finance teams don't have trouble creating a budget. The hard part is figuring out how much should go where. Should 70% of your revenue fund programs? Is 15% on admin too high? What about reserves — do you even have any?

The 50/30/20 rule gives you a starting framework to answer those questions. It was originally designed for personal finance, but the underlying principle — divide your income into essentials, growth, and savings — translates surprisingly well to nonprofit budgeting when you adapt the categories.

This guide explains how the rule works, how to translate it for nonprofit budgets, when to adjust the ratios, and how to put it into practice using QuickBooks or dedicated budgeting tools.

What Is the 50/30/20 Rule?

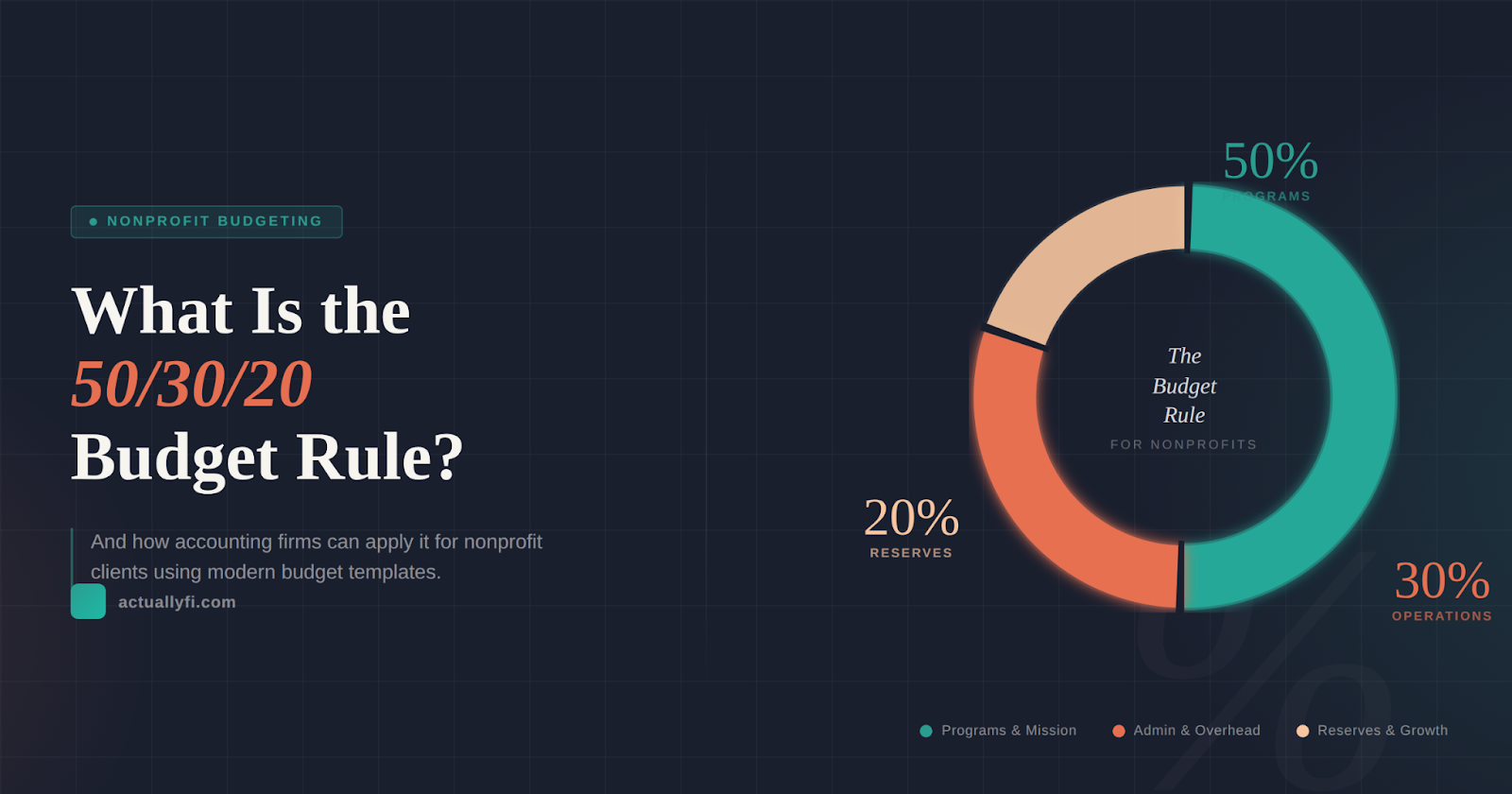

The 50/30/20 rule is a budgeting framework that divides total income into three spending categories: 50% for needs (essential operating costs), 30% for wants (strategic or discretionary spending), and 20% for savings (reserves, debt reduction, or long-term goals).

The model was popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan. It's widely used in personal finance because of its simplicity — you don't need to track every dollar, you just need to stay within the three buckets.

For nonprofits, the exact labels change but the logic holds. Instead of "needs vs. wants," think "core mission delivery vs. capacity building." Instead of "savings," think "operating reserves and financial resilience."

The beauty of this framework is that it forces a conversation most nonprofit boards avoid: how much of our budget should go to things that aren't direct program delivery? The 50/30/20 split gives you permission to invest in growth and stability without feeling like you're taking money away from the mission.

How the 50/30/20 Rule Translates to Nonprofits

Here's how each bucket maps to nonprofit operations:

50% — Core Programs and Essential Operations. This is the non-negotiable work: direct service delivery, program staff salaries, program supplies, and the infrastructure that keeps your mission running day to day. For a food bank, this is the warehouse, the trucks, and the people who pack and distribute meals. For a mentoring nonprofit, it's the coordinators, training materials, and meeting space.

30% — Mission Expansion and Capacity Building. Think of this as your "invest in the future" bucket. Marketing and communications, staff professional development, technology upgrades, new program pilots, fundraising campaigns, and strategic planning all live here. This is the spending that doesn't deliver services today but makes your organization stronger and more effective tomorrow.

20% — Financial Reserves and Stability. Operating reserves, debt reduction, building a rainy-day fund, or setting aside money for capital projects. The Nonprofit Operating Reserves Initiative recommends that nonprofits maintain at least three to six months of operating expenses in reserve. This bucket is how you build toward that.

The category that most nonprofits underinvest in is the 20% reserves bucket. There's constant pressure to show donors that "every dollar goes to the mission," but organizations without reserves are one bad quarter away from a cash crisis. The 50/30/20 framework helps you push back on that pressure with a clear rationale.

Benefits of Using the 50/30/20 Framework

It prevents the "overhead myth" trap. Nonprofits that spend 90%+ on programs often do so at the expense of staff development, technology, and fundraising capacity. Over time, this creates burnout, high turnover, and stagnant growth. The 50/30/20 split explicitly allocates room for the investments that keep an organization healthy.

It simplifies board conversations. Instead of debating individual line items, your board can discuss whether the overall allocation between programs, growth, and reserves is right for your stage. That's a more productive conversation — and one that's easier to have when everyone is looking at the same three-bucket framework.

It builds resilience. We've seen too many nonprofits scramble when a major grant ends or a fundraising event underperforms. Those with reserves absorb the shock. Those without them are laying off staff within 60 days. A consistent 20% reserve allocation prevents that.

It improves donor transparency. When you can show donors a clear, rational allocation of their contributions — half to direct programs, a third to growing capacity, and a fifth to long-term stability — most people find that reassuring rather than concerning. It signals that your organization is managed responsibly.

One caveat: this framework is a starting point, not a straitjacket. Your actual ratios should reflect your organization's stage, funding mix, and strategic priorities. We'll cover when to adjust in a later section.

How to Apply the Rule in Practice

If you're building your budget manually in a spreadsheet, the math is straightforward:

Core Programs Budget = Total Revenue × 50%

Growth & Capacity Budget = Total Revenue × 30%

Reserves Allocation = Total Revenue × 20%

Then map your expense categories into the appropriate bucket. Salaries for program staff go in the 50%. Your new website redesign goes in the 30%. The transfer to your reserve fund goes in the 20%.

The tricky part is shared costs. Your Executive Director's salary supports all three buckets. Rent keeps the lights on for programs AND administration. For these, use a reasonable allocation method — many nonprofits split shared costs proportionally based on staff time or square footage. Don't overthink it; consistency matters more than precision.

If you use QuickBooks for accounting, you can set up class tracking to tag expenses by program, growth, and reserves. This lets you run reports that show your actual allocation versus the 50/30/20 targets. See our complete guide to budgeting for nonprofits in QuickBooks for step-by-step setup instructions.

For organizations past the spreadsheet stage, Actually Finance lets you build program-level budgets following the 50/30/20 framework, track actual spending against targets in real time, and visualize your allocation breakdown on a dashboard your whole finance team can access.

When to Adjust the Ratios

The 50/30/20 split is a useful default, but not every nonprofit should follow it exactly. Your stage, funding mix, and strategic priorities should drive the actual numbers.

Early-stage nonprofits (0-3 years) often need to invest more heavily in building programs and establishing credibility. A split closer to 60-65% programs, 25% capacity building, and 10-15% reserves makes sense when you're still proving your model. You can't save 20% if you don't have sustainable revenue yet.

Growth-stage nonprofits launching new programs or expanding into new regions might temporarily shift toward 45% programs, 35% growth, and 20% reserves. The extra investment in capacity building fuels the expansion.

Established organizations with stable funding can afford to build reserves more aggressively — sometimes 25% or more, especially if they're saving for a capital project or building an endowment.

Grant-heavy nonprofits should align their reserve strategy with grant cycles. If your largest grant renews every three years, you'll want enough reserves to cover the gap period if renewal is delayed or denied. That might mean 25% reserves during the grant period to build a cushion.

The key principle: adjust intentionally, not reactively. Decide your ratios at the start of the fiscal year based on your strategic plan, then monitor them quarterly. Don't let the ratios drift because nobody was paying attention.

The Bottom Line

The 50/30/20 rule gives nonprofits something they rarely have: a simple, defensible framework for budget allocation. Fund your mission first (50%), invest in your organization's future (30%), and build the financial cushion that keeps you resilient through the inevitable ups and downs (20%).

It won't answer every budget question. But it will move your team past the endless line-item debates and toward the strategic conversation that actually matters: are we allocating our resources in a way that serves both our mission today and our sustainability tomorrow?

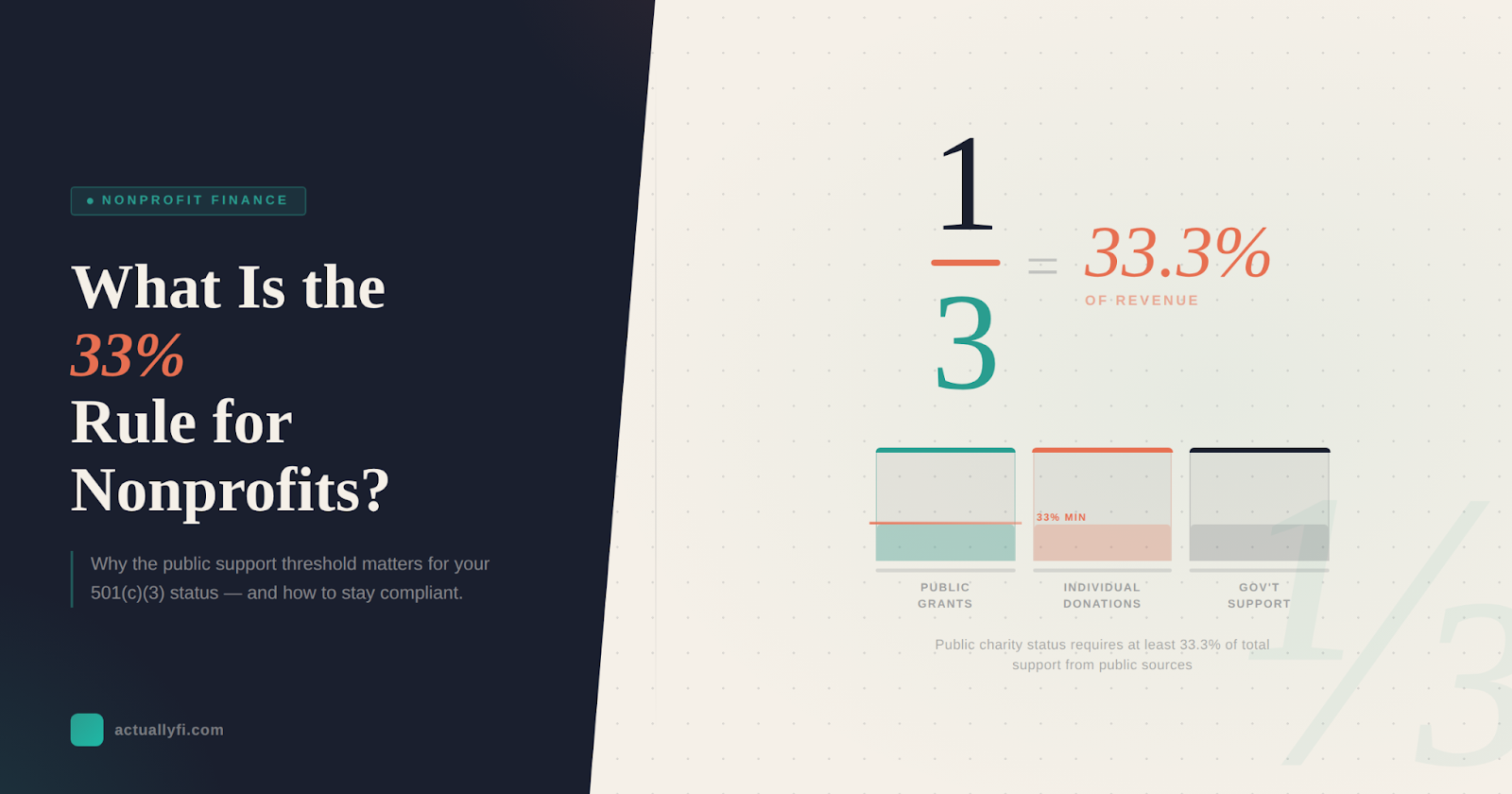

Make sure your funding sources meet compliance requirements too. Read about the 33% public support test for nonprofits.

Frequently Asked Questions

Can nonprofits use the 50/30/20 rule for grant budgeting?

You can use it as a strategic guideline, but individual grant budgets need to follow funder requirements first. Most grants specify allowable costs and indirect cost rates that override any internal allocation framework. Where the 50/30/20 rule helps is in your organizational budget — the overall plan for how all revenue (grants, donations, earned income) gets allocated across your programs, growth investments, and reserves. Think of it as the forest view while grant budgets are individual trees.

What is the difference between the 50/30/20 rule and program budgeting?

They work at different levels. The 50/30/20 rule is a high-level allocation framework that answers "how should we divide our total resources?" Program budgeting goes deeper, assigning specific dollar amounts to individual programs, grants, or initiatives. Most nonprofits use both: the 50/30/20 split as a strategic compass and program budgets for detailed operational planning. They complement each other rather than competing.

Is the 50/30/20 rule required for nonprofits?

No. There's no IRS requirement or accounting standard that mandates this specific allocation. It's a management tool, not a compliance obligation. Your board and leadership should adapt the percentages to fit your organization's stage, mission, funding mix, and strategic goals. Some organizations use different frameworks entirely — the important thing is having some intentional allocation strategy rather than budgeting purely by inertia.

How do I adjust the 50/30/20 split for a startup nonprofit?

Startup nonprofits typically need more resources directed at program development and proving their model. A common early-stage split is 60-70% on programs and initial operations, 20% on capacity building and fundraising infrastructure, and 10-15% on building initial reserves. As you secure more stable funding and your programs mature, gradually shift toward the standard 50/30/20 balance. The transition usually happens over 3-5 years as the organization stabilizes.

David Cristello

.svg)

About the Author

David Cristello is the Co-Founder of Actually Finance. He's been an entrepreneur in the accounting and nonprofit space for over 10 years, previously building a company that made the Inc5000 list

.png)

.webp)