- Why Salary Allocations Matter in Nonprofit Accounting

- How Nonprofits Allocate Payroll Across Programs and Grants

- Payroll Journal Entries for Nonprofits: Real Examples

- Common Payroll Allocation Mistakes That Create Reporting Problems

- How to Reconcile Payroll Journal Entries for Nonprofits

- Conclusion

Table of contents

Last updated: June 1, 2026

Payroll is often the largest expense category in a nonprofit budget. While recording payroll itself is straightforward, allocating salary costs across multiple programs, grants, and funding sources is where many organizations encounter challenges.

A program director may split time between three grants. An executive director may oversee several departments. Administrative staff often support multiple initiatives simultaneously. Without accurate payroll allocations, financial reports, grant budgets, and reimbursement requests can become unreliable.

This guide explains how payroll journal entries for nonprofits work, how salary allocations should be handled, and how nonprofit finance teams can improve reporting accuracy while reducing manual spreadsheet work.

Key Takeaways

- Payroll journal entries record wages, taxes, benefits, and payroll liabilities.

- Nonprofits often allocate salaries across multiple programs and grants.

- Allocation methods should be documented and consistently applied.

- Timesheets and effort reporting improve allocation accuracy.

- Payroll allocations directly affect grant reporting and reimbursement requests.

- Proper payroll tracking improves budget visibility and compliance.

What Are Payroll Journal Entries for Nonprofits?

Payroll journal entries record payroll-related transactions in the general ledger.

These entries typically include:

- Gross wages

- Payroll taxes

- Employee benefit costs

- Employer tax expenses

- Payroll liabilities

- Net payroll payments

Unlike for-profit businesses, nonprofits often need additional reporting by:

- Program

- Grant

- Funding source

- Department

- Restricted fund

This means payroll expenses must often be divided among several categories instead of being posted to a single expense account.

For many organizations, payroll allocations become essential because grant agreements frequently require detailed reporting showing how salary costs support specific programs.

Why Salary Allocations Matter in Nonprofit Accounting

Many nonprofit employees work across multiple initiatives.

For example:

- A program manager may oversee two grant-funded programs.

- An executive director may support fundraising, administration, and programs.

- A finance manager may provide services to every department.

If payroll costs are charged entirely to one program, financial reports become distorted.

Accurate salary allocations help nonprofits:

- Track true program costs

- Support grant reimbursement requests

- Improve budget accuracy

- Meet audit requirements

- Produce reliable board reports

- Monitor grant spending

Funders increasingly expect organizations to demonstrate how payroll expenses relate to grant activities. Well-documented payroll allocations help provide that evidence.

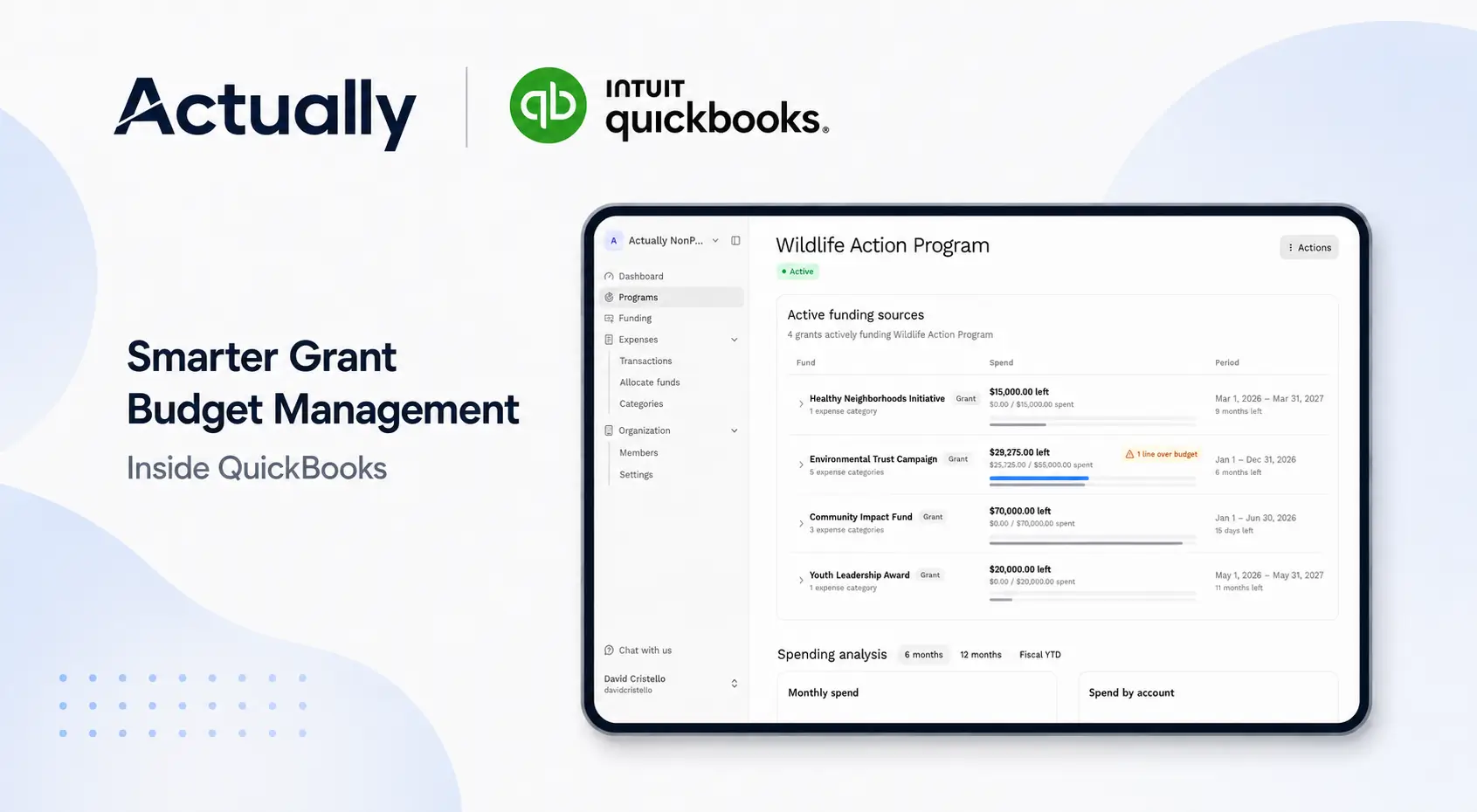

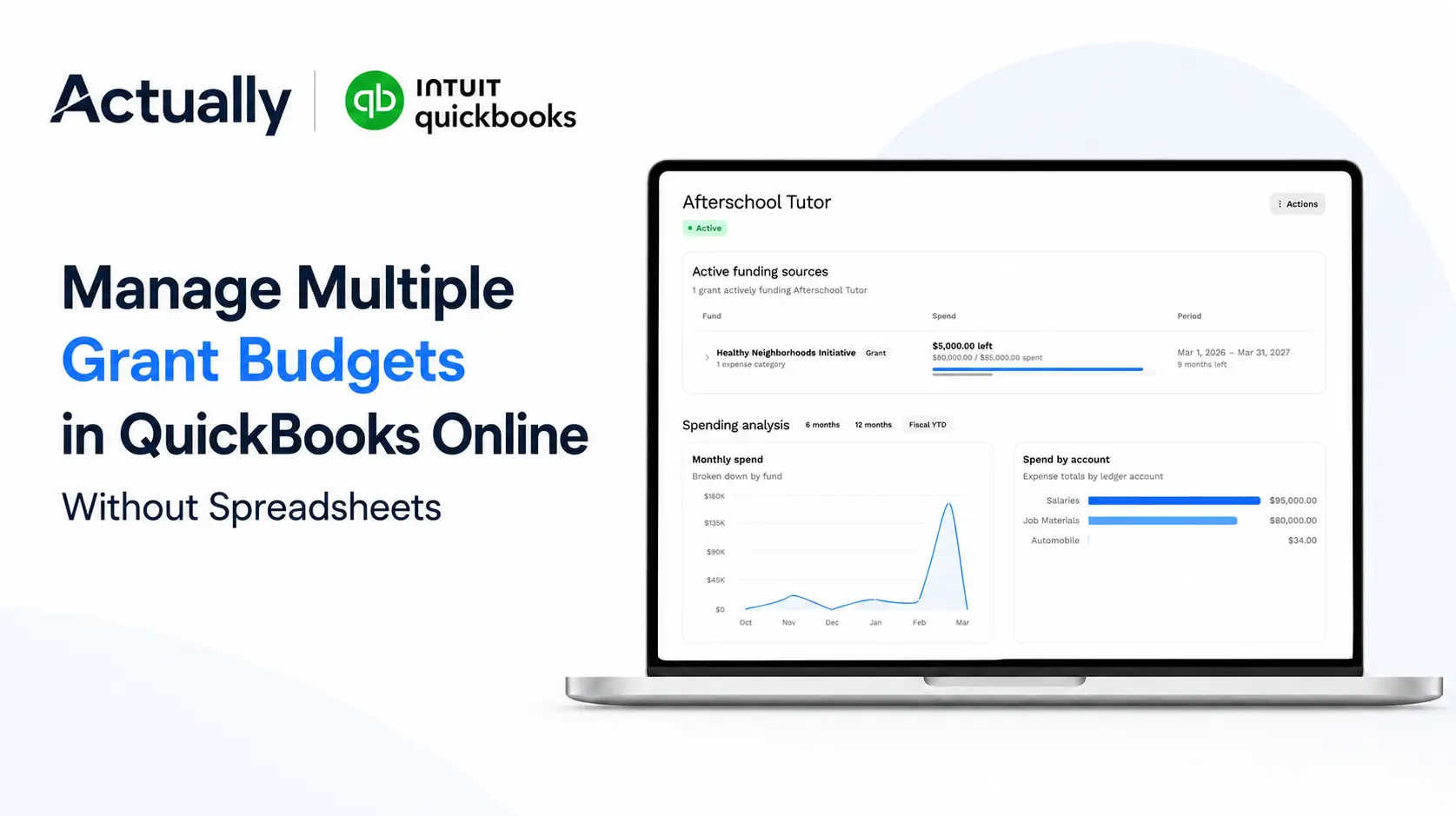

How Nonprofits Allocate Payroll Across Programs and Grants

Most nonprofits use one of several common allocation methodologies.

Percentage-Based Allocations

Some organizations allocate payroll based on predetermined percentages.

Example:

If the monthly salary is $6,000:

- Program A receives $3,000

- Program B receives $1,800

- Administration receives $1,200

This approach is common when employee responsibilities remain relatively stable throughout the year.

Timesheet-Based Allocations

Many grant-funded organizations require employees to track actual hours worked.

Example:

Total Hours = 160

Allocation:

- Housing Program = 50%

- Youth Program = 25%

- Administration = 25%

This method often provides stronger audit support because allocations are based on documented activity.

Effort Reporting

Some federally funded nonprofits use effort certification reports to document how employees spend their time.

These reports help demonstrate that payroll costs charged to grants align with actual work performed.

Payroll Journal Entries for Nonprofits: Real Examples

Consider a nonprofit employee with:

- Gross salary: $5,000

- Employee taxes withheld: $750

- Net payroll: $4,250

Initial Payroll Entry

The next step is allocating the salary expense.

Payroll Allocation Entry

Assume:

- Grant A = 60%

- Grant B = 25%

- Administration = 15%

This allocation ensures program-level reports accurately reflect labor costs.

Allocating Benefits and Payroll Taxes

Payroll allocations should not stop with wages.

Organizations should also allocate:

- Employer payroll taxes

- Health insurance

- Retirement contributions

- Workers compensation

- Other employee benefits

Many nonprofits overlook these expenses, causing grant reports to understate actual personnel costs.

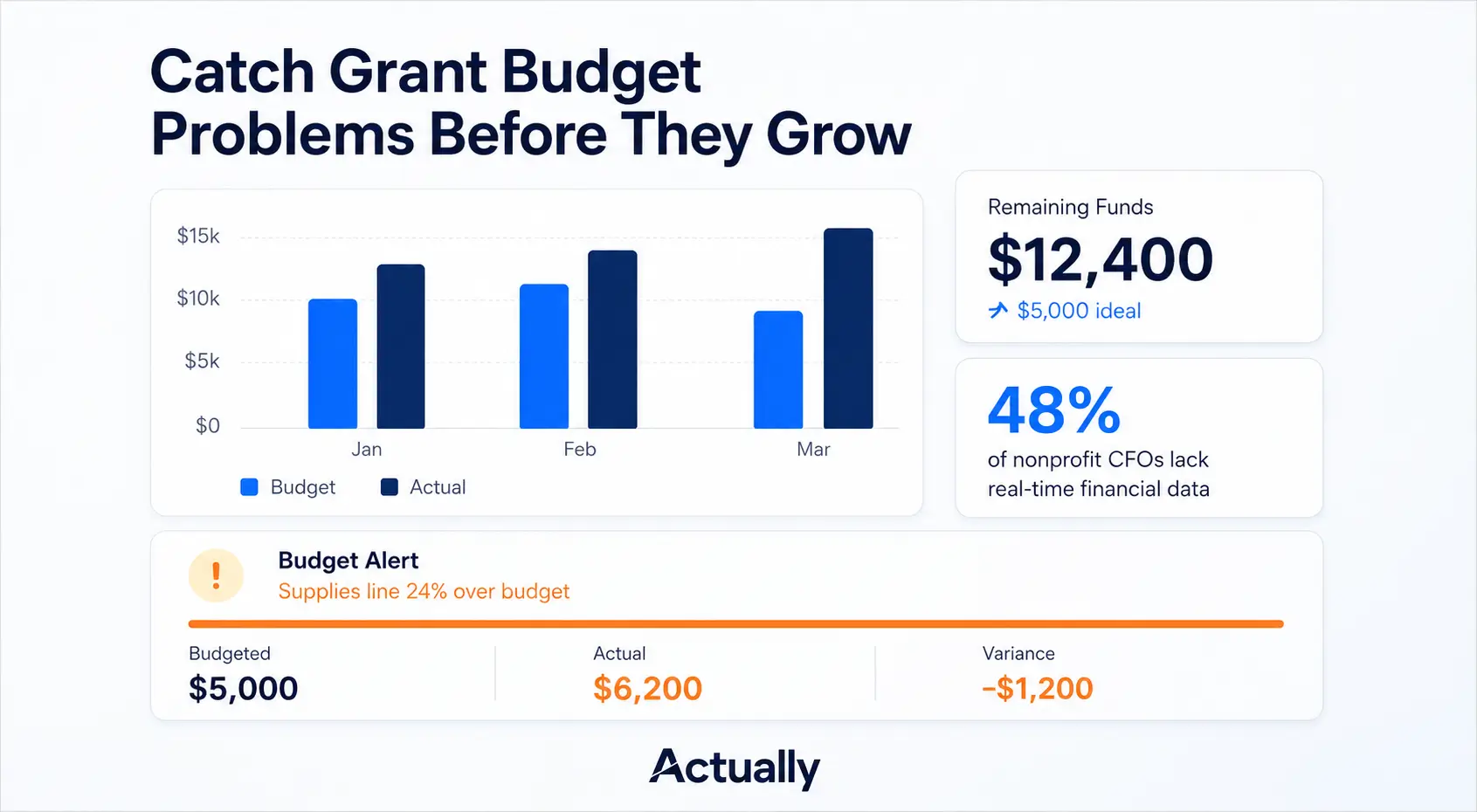

Common Payroll Allocation Mistakes That Create Reporting Problems

Using Estimates Without Documentation

Allocations should be supported by:

- Timesheets

- Effort reports

- Workload analysis

- Management approval

Undocumented estimates can create audit concerns.

Forgetting Employer Payroll Costs

Organizations sometimes allocate salaries but forget:

- Payroll taxes

- Benefits

- Retirement contributions

This results in incomplete program costs.

Applying the Same Percentages Forever

Employee responsibilities change over time.

Allocations should be reviewed regularly to ensure they continue reflecting actual work performed.

Mixing Restricted and Unrestricted Activities

Grant-funded activities should remain clearly separated from unrestricted operational work.

Proper payroll allocations help maintain this distinction.

Relying on Complex Spreadsheets

As nonprofits grow, payroll allocation spreadsheets become harder to maintain.

Common issues include:

- Formula errors

- Broken links

- Version control problems

- Duplicate calculations

- Reporting delays

Many organizations eventually seek more centralized reporting workflows to reduce spreadsheet dependency.

How to Reconcile Payroll Journal Entries for Nonprofits

Payroll reconciliation should occur monthly.

Finance teams should verify:

- Payroll registers match journal entries

- Salary allocations match approved methodologies

- Grant reports align with payroll allocations

- Payroll liabilities are accurate

- Benefits are allocated correctly

- Budget reports reflect payroll expenses properly

A simple monthly review can identify allocation issues before they affect funder reports or year-end audits.

Payroll Reconciliation Checklist

- Verify payroll totals

- Review allocation percentages

- Compare payroll reports to grant budgets

- Confirm benefit allocations

- Review payroll liabilities

- Investigate unusual variances

- Update allocation methodologies if necessary

Organizations that reconcile payroll regularly typically experience fewer reporting surprises and stronger audit outcomes.

Conclusion

Payroll journal entries for nonprofits involve much more than recording wages and taxes. For organizations managing multiple programs and grants, payroll allocations play a critical role in financial reporting, grant compliance, budgeting, and reimbursement requests.

The most effective nonprofits establish documented allocation methodologies, review payroll allocations regularly, and ensure personnel costs are accurately distributed across funding sources.

As organizations grow, centralized budgeting and reporting tools can help reduce manual processes and improve visibility into labor costs across programs and grants.

Understanding payroll journal entries and salary allocation workflows is one of the most practical steps nonprofits can take toward stronger financial management.

Frequently Asked Questions

What are payroll journal entries for nonprofits?

Payroll journal entries for nonprofits are accounting records that document wages, payroll taxes, benefits, and payroll liabilities. They help organizations accurately track labor costs across programs, grants, and administrative activities.

How do nonprofits allocate salaries across multiple grants?

Most nonprofits allocate salaries using percentage-based allocations, timesheets, effort reporting, or documented cost allocation plans. The chosen method should be applied consistently and supported by documentation.

Can QuickBooks Online track payroll allocations by program?

Yes. QuickBooks Online can track payroll expenses by Classes, Locations, or other reporting structures. Many nonprofits use additional budgeting and reporting tools to improve visibility across grants and programs.

Why are payroll allocations important for grant reporting?

Payroll costs are often the largest expense in nonprofit budgets. Accurate allocations help organizations demonstrate how grant funds are used, support reimbursement requests, and improve reporting accuracy.

Should employer payroll taxes and benefits be allocated to grants?

Yes. In addition to salaries, nonprofits should allocate employer payroll taxes, health insurance, retirement contributions, and other employee benefits when appropriate. This provides a more accurate view of total personnel costs.

What is the best method for allocating payroll expenses?

There is no single method that works for every organization. Common approaches include percentage-based allocations, timesheet tracking, effort reporting, and cost allocation plans. The best method depends on grant requirements and organizational complexity.

How often should payroll allocations be reviewed?

Payroll allocations should be reviewed at least monthly. Employee responsibilities can change over time, and regular reviews help ensure allocations remain accurate and compliant.

How can nonprofits reduce spreadsheet-based payroll tracking?

Many nonprofits centralize payroll allocations, grant budgeting, and reporting workflows using tools that integrate with QuickBooks Online. This reduces manual calculations, reporting errors, and version-control issues.

David Cristello

.svg)

About the Author

David Cristello is the Co-Founder of Actually Finance. He's been an entrepreneur in the accounting and nonprofit space for over 10 years, previously building a company that made the Inc5000 list

.png)

.webp)